4 Components Approach to Managing Apparent Losses

How to Squeeze the Lost Revenue Box

LEAKSSuite Library Update 21st August 2019:

This Webpage is limited to a very brief introduction to the topic of Apparent (Commercial) water losses, as all relevant material previously published in the Apparent Losses Section of the former LEAKSSuite website (2015 onwards) was transferred to the Apparent Losses Section of the Malta College of Arts, Science and Technology mcast.edu.mt/apparent-losses during 2018. The MCAST website provides links to

- Free Guidance Notes on Apparent Losses and Water Loss Reduction Planning: Authors Michel Vermersch, Fatima Carteado, Alex Rizzo, Edgar Johnson, Francisco Arregui, Allan Lambert.

The Guidance Notes format of 1 main document and 9 Appendices, which allows each of the 10 documents to be updated separately in future, or additional Appendices added. Any future changes will be documented on the MCAST website. The Guidance Notes main document contains Sections on Water Balance and Apparent Losses; Water Audit Component Analysis; Apparent Losses Indicators; Action Planning and Dynamics of Losses; and Economics of Apparent Losses. Each of the Sections has a set of References (some with weblinks to free papers). The Bibliography lists 74 papers and books. Each of the Appendices also has its own set of References. By the time the Guidance Notes were transferred to MCAST, they had been accessed over 3,200 times on the LEAKSSuite website in 3 years…

- Free papers by leading International Experts on Apparent Losses: these authors strongly support the policy of LEAKSuite Library in promoting easy free access to their presentations and papers at Conferences and Workshops, and to technical Guidance notes. Assignment of copyright to publishers requiring significant limits to be placed on such open access is actively avoided. There are over 20 such papers already available on the MCAST website, and authors who are interested in contributing, free to all, are invited to contact Alex Rizzo, Michel Vermersch or Fatima Carteado who have agreed to review, recommend and add additional high quality material on Apparent Losses in this section of the MCAST website.

The following paragraphs are a very brief introduction to Apparent Losses.

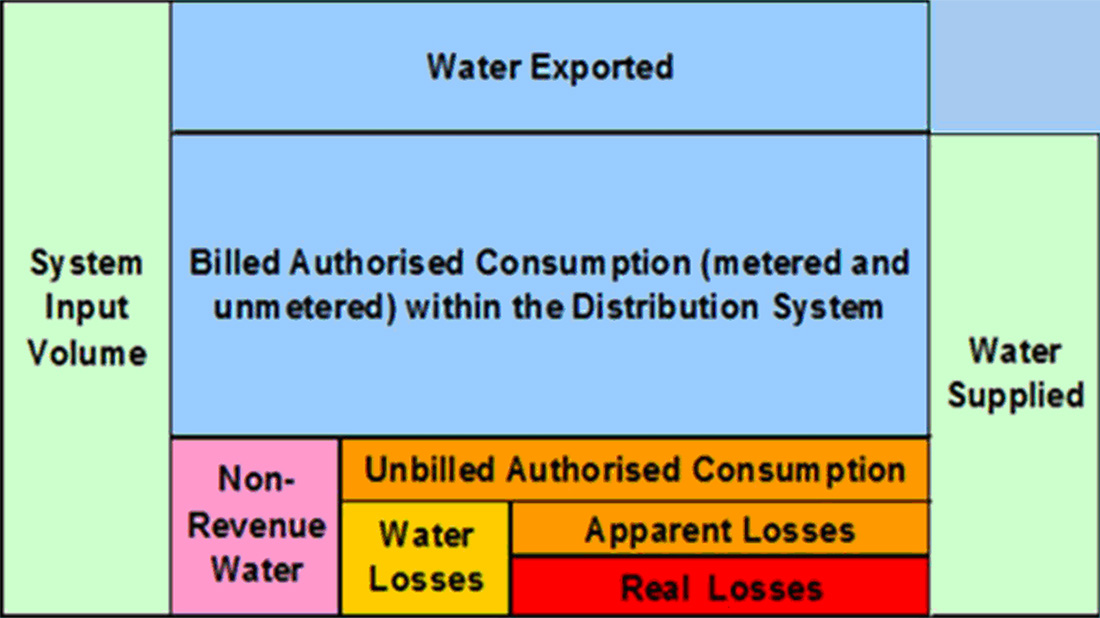

Non-Revenue Water consists of Unbilled Authorised Consumption, Apparent Losses and Real Losses. Apparent Losses (also known as Commercial Losses) result in lost revenue for Utilities, as they consist of unauthorised consumption (theft or illegal use), and all types of inaccuracies associated with production metering and customer metering. Errors in assessment of Apparent Losses may lead to errors in estimation of Real Losses and erroneous approaches in planning for Non-Revenue Water reduction.

In order to reduce both Apparent and Real Losses in a sustainable way, it is necessary to build appropriate action planning models to control Non-Revenue Water as a whole. NRW reduction involves the control of a large number of components. Apparent Losses reduction requires many types of expertise, not only in technical and operational fields but also in human, social and management fields.

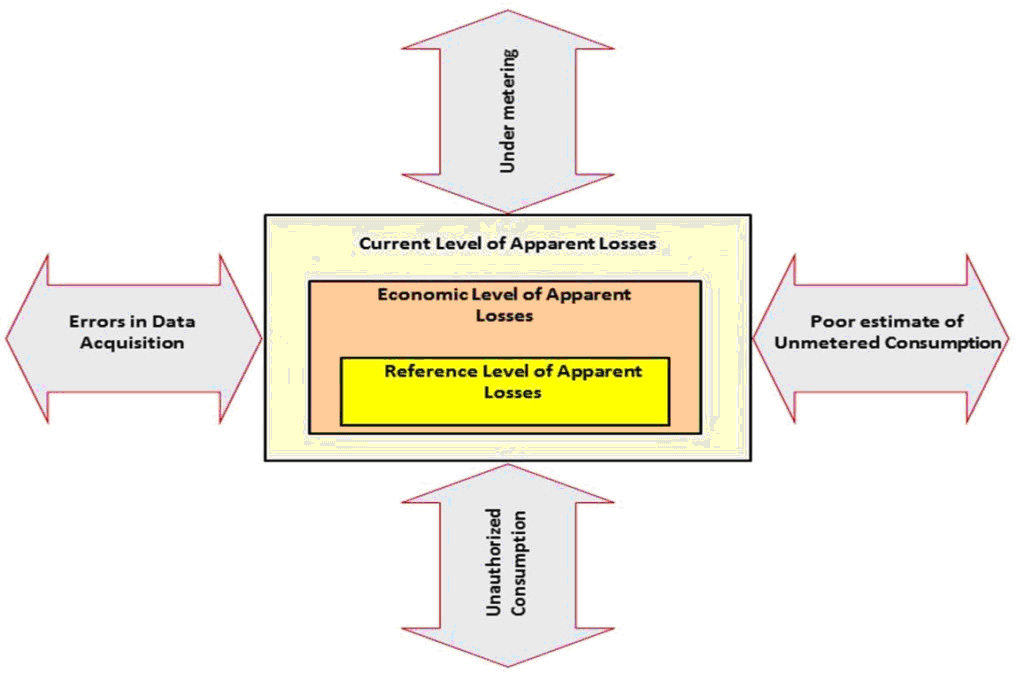

The diagram below was developed by the Apparent Losses Initiative, which was launched by the International Water Association in November 2007. It is now widely used internationally as a simple means of explaining the four basic categories of activity that need to be under control for effective operational management of Apparent Losses.

The area of the large rectangle represents the Current Annual Apparent Losses, in volume per year, for any specific system. The intermediate rectangle represents the Economic Level of Apparent Losses, which is a combination of the various economic levels for the four categories of action. Finally, the small rectangle represents a Reference Level of Apparent Losses, which is based on the performance of well-managed Utilities worldwide.

The four main categories of actions to get Apparent Losses under control are listed below with a non-exhaustive list of activities that may be included under these categories.

Data Acquisition errors: data capture, data transmission, data processing, meter reading procedures, meter reading procedures, automatic meter reading (AMR), supervisory control and data acquisition (SCADA) etc.

Water Meter errors: installation and calibration procedures for large meters, calculation of the average weighted error (AWE) for customer meters, selection of customer meters, consumption profiles, meter sizing, meter installation, meter aging, optimum replacement period, comprehensive and/or targeted replacement programs, etc.

Errors in Unmetered Consumption estimates: overall metering policy (this component may be important when a significant number of customers are not metered).

Unauthorized Consumption: detection of unregistered connections and detection of frauds on registered connections, overall customer census, targeted customer census, communication policy, improvement of customer management procedures, etc.

Each category of action is represented as a 2-way arrow. If the Utility implements the corrective action, the relevant loss will be reduced. If the Utility does not, the AL box will expand and Apparent Losses will increase. Each category of losses has a natural rate of rise.If each of the four management components is applied at an economic level of activity (with priority being given to those with the quickest payback period or highest benefit/cost ratio), the Apparent Losses volume should eventually reduce to an economic level of Apparent Losses (shown as the small rectangle). This technique, which is also applied to management of Real Losses, is known as ‘squeezing the box’.

It is essential to get all four categories of Apparent Losses under control: if the Utility only puts the stress on a single category, the relevant Apparent Losses component may decrease, but the losses generated by the other categories that are not under control will continue to increase. Despite the implemented action, the total Apparent Losses may not change or may even continue to increase. In some specific cases, it appears that the levels of Real Losses and Apparent Losses are linked together. Thus, a combined approach is necessary to get both categories of loss under control (dynamics of loss)